How to Build a 6-Month Emergency Fund in 2026

An emergency fund is one of the most important financial tools for protecting yourself from unexpected expenses. Learn how to calculate your target amount, where to keep your savings, and the step-by-step process for building a six-month emergency fund in 2026. Whether you're just starting your financial journey or strengthening your financial security, this guide will help you create a solid safety net.

Table of Contents

- Quick Answer

- What Is an Emergency Fund?

- Why It Matters

- How Much Should You Save?

- Three Months of Expenses

- Six Months of Expenses

- Twelve Months of Expenses

- How to Calculate Your Emergency Fund

- Where Should You Keep Your Emergency Fund?

- High-Yield Savings Account

- Money Market Account

- Traditional Savings Account

- Where Not to Keep Emergency Savings

- Stocks

- Cryptocurrency

- Long-Term Investments

- Checking Accounts

- Benefits of a 6-Month Emergency Fund

- Financial Security

- Less Stress

- Avoiding Debt

- Greater Flexibility

- Step-by-Step Guide

- Step 1: Set Your Target

- Step 2: Open a Dedicated Savings Account

- Step 3: Start Small

- Step 4: Automate Contributions

- Step 5: Increase Contributions Over Time

- Step 6: Leave the Money Alone

- Real-Life Example

- Common Mistakes

- Investing Emergency Savings

- Waiting for the Perfect Time

- Using the Fund for Non-Emergencies

- Keeping Too Little Cash

- Ignoring Inflation

- Frequently Asked Questions

- Is a 6-Month Emergency Fund Necessary?

- Should I Invest Before Building an Emergency Fund?

- Where Is the Best Place to Keep an Emergency Fund?

- Can I Use My Emergency Fund for Vacations?

- What If I Can't Save Six Months of Expenses?

- Bottom Line

- Related Articles

- Recommended Categories

How to Build a 6-Month Emergency Fund in 2026

Building wealth is important, but before investing in stocks, ETFs, or retirement accounts, most financial experts recommend creating an emergency fund.

Why?

Because unexpected expenses are inevitable.

A job loss, medical bill, car repair, or home emergency can quickly derail your finances if you're not prepared.

An emergency fund acts as a financial safety net, helping you cover unexpected costs without relying on credit cards, loans, or withdrawing money from long-term investments.

In 2026, with economic uncertainty and rising living costs, having a properly funded emergency account is more important than ever.

Quick Answer

A 6-month emergency fund is a cash reserve that covers six months of essential living expenses.

Most financial experts recommend keeping emergency savings in a safe and accessible account, such as a high-yield savings account.

For many households, building this fund should be a higher priority than investing aggressively.

What Is an Emergency Fund?

An emergency fund is money set aside specifically for unexpected financial situations.

It is not:

-

Vacation money

-

Investment capital

-

Holiday spending

-

Home renovation savings

Instead, it's reserved for genuine emergencies.

Examples include:

-

Job loss

-

Medical expenses

-

Major car repairs

-

Emergency travel

-

Unexpected home repairs

The purpose is to provide financial stability during difficult situations.

Why It Matters

Many Americans live paycheck to paycheck.

Without emergency savings, even a relatively small unexpected expense can create financial stress.

A strong emergency fund helps you:

-

Avoid credit card debt

-

Prevent high-interest borrowing

-

Protect long-term investments

-

Reduce financial anxiety

-

Improve overall financial security

An emergency fund gives you options when life doesn't go according to plan.

How Much Should You Save?

The most common recommendation is:

Three Months of Expenses

Suitable for:

-

Dual-income households

-

Stable employment situations

-

Lower financial obligations

Six Months of Expenses

Suitable for:

-

Most individuals and families

-

Single-income households

-

Moderate job security

Twelve Months of Expenses

Suitable for:

-

Self-employed workers

-

Freelancers

-

Business owners

-

Individuals with variable income

For most people, six months is an excellent target.

How to Calculate Your Emergency Fund

Start by calculating your essential monthly expenses.

Include:

-

Housing

-

Utilities

-

Food

-

Insurance

-

Transportation

-

Minimum debt payments

Example:

| Expense | Monthly Cost |

|---|---|

| Rent | $1,500 |

| Utilities | $200 |

| Food | $500 |

| Insurance | $300 |

| Transportation | $300 |

| Debt Payments | $200 |

Total Monthly Expenses = $3,000

Six months of expenses:

$3,000 × 6 = $18,000

Your emergency fund target would be approximately $18,000.

Where Should You Keep Your Emergency Fund?

The best emergency fund location should provide:

-

Safety

-

Liquidity

-

Accessibility

High-Yield Savings Account

For most people, this is the best option.

Benefits:

-

FDIC insurance

-

Easy access

-

Competitive interest rates

-

No market risk

Money Market Account

Another safe alternative that may offer competitive yields.

Traditional Savings Account

Acceptable, but often offers lower interest rates.

Where Not to Keep Emergency Savings

Stocks

The market could decline exactly when you need the money.

Cryptocurrency

Volatility can make crypto unsuitable for emergency savings.

Long-Term Investments

Emergency funds should remain accessible.

Checking Accounts

While convenient, they often provide little to no interest.

Benefits of a 6-Month Emergency Fund

Financial Security

Unexpected events become easier to manage.

Less Stress

Money problems are a major source of anxiety.

Emergency savings can reduce that burden.

Avoiding Debt

Many people rely on credit cards during emergencies.

An emergency fund helps break that cycle.

Greater Flexibility

You can make decisions based on what's best rather than what's financially urgent.

Step-by-Step Guide

Step 1: Set Your Target

Calculate six months of essential expenses.

Step 2: Open a Dedicated Savings Account

Separate emergency savings from everyday spending.

Step 3: Start Small

Don't focus on the final goal immediately.

Even saving:

-

$500

-

$1,000

-

$2,000

creates valuable protection.

Step 4: Automate Contributions

Set up recurring transfers.

Automation removes the need for constant decisions.

Step 5: Increase Contributions Over Time

Whenever income rises, increase savings contributions.

Step 6: Leave the Money Alone

Only use emergency savings for genuine emergencies.

Real-Life Example

Imagine John spends approximately $3,500 per month on essential expenses.

His emergency fund target becomes:

$3,500 × 6 = $21,000

John decides to save:

$500 per month

At that rate, he reaches his goal in approximately three and a half years.

Along the way, each dollar saved improves his financial security.

Even before reaching the full target, he becomes increasingly protected from unexpected events.

Common Mistakes

Investing Emergency Savings

Emergency money should remain stable and accessible.

Waiting for the Perfect Time

Many people postpone saving because they feel they can't save enough.

Starting small is better than waiting.

Using the Fund for Non-Emergencies

Vacations and shopping are not emergencies.

Keeping Too Little Cash

A few hundred dollars may not provide adequate protection.

Ignoring Inflation

Review your emergency fund periodically to ensure it still covers your expenses.

Frequently Asked Questions

Is a 6-Month Emergency Fund Necessary?

For most households, yes. It provides a strong financial safety net.

Should I Invest Before Building an Emergency Fund?

Most experts recommend establishing emergency savings before investing aggressively.

Where Is the Best Place to Keep an Emergency Fund?

A high-yield savings account is often the best combination of safety and accessibility.

Can I Use My Emergency Fund for Vacations?

No. Emergency funds should only be used for genuine financial emergencies.

What If I Can't Save Six Months of Expenses?

Start with smaller goals such as $500, $1,000, or one month of expenses and build from there.

Bottom Line

A 6-month emergency fund remains one of the most important financial goals in 2026.

Before focusing on investment returns, retirement accounts, or stock market opportunities, it's essential to build a strong financial foundation.

Emergency savings provide security, flexibility, and peace of mind when unexpected expenses arise.

The best time to start building your emergency fund was yesterday.

The second-best time is today.

Related Articles

-

High-Yield Savings Accounts: Are They Worth It in 2026?

-

How Much Money Should You Save Each Month?

-

The 50/30/20 Budget Rule Explained

Recommended Categories

-

Saving Money

-

Personal Finance

-

Budgeting

Frequently Asked Questions

Common questions about saving money.

Written by

FPG Editorial Team

Personal finance writers, editors and fact-checkers. Read about our editorial standards.

Share this article

Related Articles

The Best Budgeting Apps of 2026: Mastering Your Money in the Digital Age

Navigating personal finance in 2026 requires more than just a spreadsheet. We review the top budget apps helping Americans combat inflation and reach financial independence today.

Read More

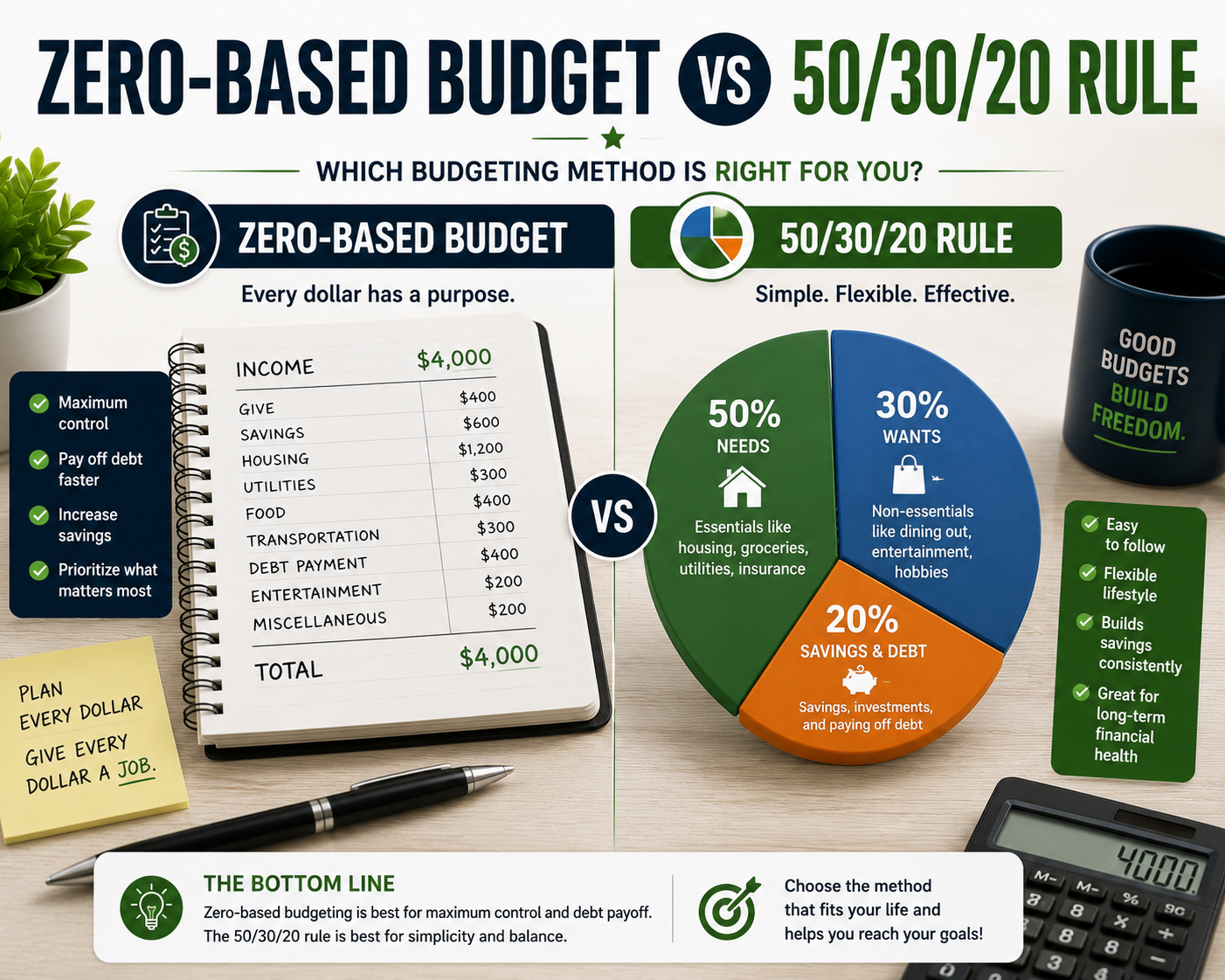

Zero-Based Budget vs. 50/30/20 Rule: Choosing the Best Framework for 2026

In the evolving economic landscape of 2026, choosing between a Zero-Based Budget and the 50/30/20 Rule depends on your financial granularity. Discover which system offers the stability you need.

Read More

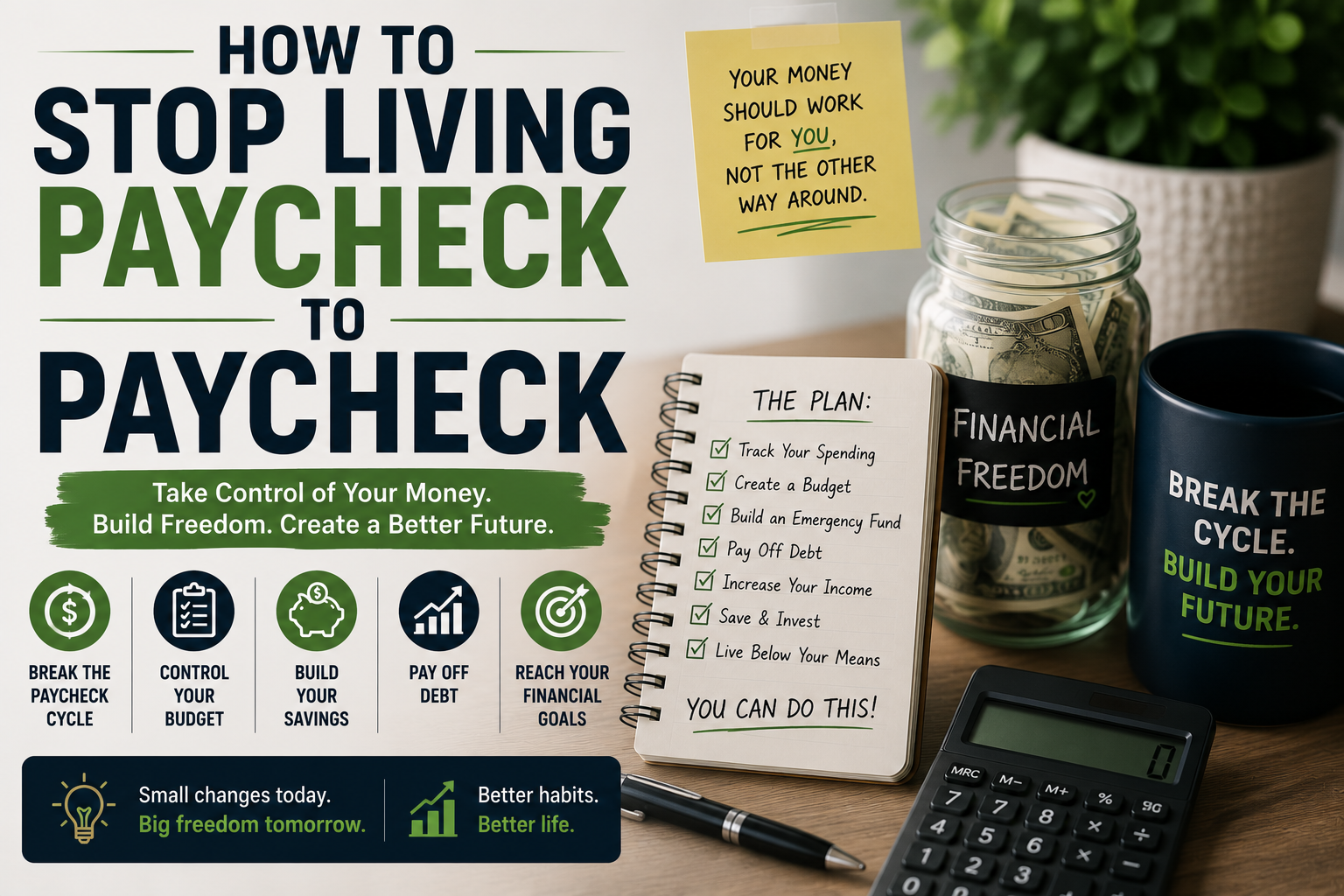

How to Stop Living Paycheck to Paycheck: A Strategic Financial Guide for 2026

Living paycheck to paycheck remains a reality for more than half of Americans. In 2026, shifting economic landscapes require a tactical approach to cash flow management, automated savings, and strategic debt reduction to secure lasting financial freedom.

Read MoreRecommended Guides

Pick a financial goal and follow our step-by-step roadmap.

Popular Resources

Free calculators, templates and trusted finance tools.

Join Thousands of Readers Building Wealth Smarter

Get weekly financial insights, investing strategies, money-saving tips, and wealth-building guidance delivered directly to your inbox.

- Double opt-in

- No spam, ever

- Unsubscribe anytime